To stay more or less loans in Phil Campbell in laws, triple you to yearly profile so you can calculate about a 3rd of earnings – it means so you’re able to easily manage an effective $350K home, you would should make as much as $90,000

- Income to cover the good $350K family

- Choosing facts

- Stay the class

The latest median family sale speed since September is $394,3 hundred, depending on the Federal Organization out of Real estate professionals. However, median form 1 / 2 of sold for lots more, and you will half of for less – there are many homes within the nation that are promoting for about $350,000.

Just how much do you need to earn to fund a great domestic that’s $350,000, even in the event? That can rely on a great amount of affairs, including the quantity of their down-payment plus the rate of interest of one’s home loan. This is how to determine the amount of money necessary for an effective $350K home.

Income to afford a $350K house

To figure out exactly how much you ought to secure having good $350,000 household purchase, start with the fresh new laws. That it guideline states that you shouldn’t save money than simply twenty-eight percent of your own gross month-to-month income towards the construction will cost you, and that you ought not to spend more than thirty-six % for the all of the personal debt joint, and housing.

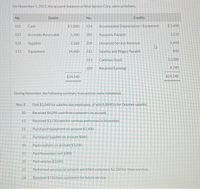

Bankrate’s mortgage calculator makes it possible to figure out how a $350,000 pick stops working. Incase a 20 percent down-payment into the a thirty-seasons home loan at an effective eight.5 percent interest rate, new month-to-month prominent and you may appeal payments started to $1,957. Do not forget to through the fees that differ according to in your geographical area, such as for instance property taxation, homeowners insurance and you can potential HOA fees. Let us round you to $step 1,957 doing $2,five hundred to help you take into account the individuals.

Proliferate one payment of $dos,500 by the several and you’ve got an annual houses costs away from $30,000. (Yet not, bear in mind that so it formula does not include their deposit and you will closing costs, which are paid off initial.)

Since the $350,000 try beneath the federal average home price, the choices would-be a little far more minimal than just they might getting within a top price point. But where you’re looking to purchase makes a positive change here: Your financial allowance goes such then in a few markets than others. For instance, the fresh average family price during the Houston try alongside your target speed at the $328,000 inside Sep, centered on Redfin study. For the San diego, regardless if, in which it was up to $900,000, you won’t rating nearly normally for your money.

To purchase a house is a pricey procedure, as there are so much a great deal more to look at than simply the brand new home’s record price. Besides your yearly income, here are additional factors one impression exactly how much family you might afford:

To keep approximately into the code, triple you to yearly shape in order to estimate regarding a 3rd of your own money – which means to help you comfortably manage a good $350K household, you’d should make around $90,000

- Credit history: Increased credit history makes it possible to be eligible for a low notice speed readily available. Even a little difference between rates will save you thousands of dollars across the life of your home mortgage.

- Deposit: A 20 percent downpayment is actually conventional, but many home loan points don’t require you to definitely establish that much. Although not, the more you can set out upfront, the low the monthly obligations might be, and you may 20% will assist you to end paying getting individual financial insurance policies.

- Debt-to-income proportion: Your DTI is where much you owe in financial trouble from inside the family in order to exactly how much you have made, conveyed since a portion (believe the next count in that signal). The low your own DTI, the much more likely lenders is always to accept you having an excellent financing.

- Loan-to-well worth proportion: Also, the LTV try a measure of the loan count for the relatives so you can how much the house or property deserves. Straight down is also best for it metric, about eyes out of a loan provider.